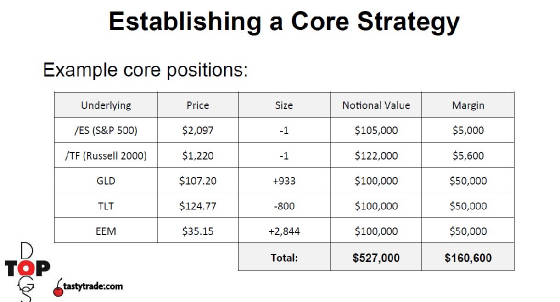

So, in the above portfolio, we used about $160,000 in buying

power to control the $500,000 worth of stuff - since we started with $250,000 in this case, this leaves about $90,000 of unused

capital. Since we are leveraged, and also to save some for future opportunities or problems, we don't want to use

all of this 'extra' capital.

Let's assume about one third is used, that is about $30,000. We will use this

to make other trades 'around' our Core Portfolio. Here are some considerations:

1. In order for the probabilities to have enough space to normalize, we need many occurrences - maybe 300 or more annually

2. Each occurrence should be small so as to reduce the risk of a single trade going against us having too much of an impact

on our portfolio (Security Risk)

3. We should have underlyings

that are not correlated so that each is a true 'occurence' and not just a 'bigger' occurence

4. We should be long and short different things to mitigate a bit of risk (Market Risk)

5. Maybe a 'Delta Neutral' or 'Lean Short" or 'Lean Long' type of mentality

The Trades could be split between Defined Risk and Undefined risk as a good balance

1. Undefined Risk have a higher winning percentage

and yield, but carry more risk

2. Defined Risk are not as efficent,

but carry a known Max loss amount

Here are examples of each: